Creating an Opening Balance Sheet from the bookkeeping software, correctly (Part 5 of Founding a Company)

Introduction

In this fifth article - if you have not read it, start with the first article - I continue telling you about the highlights of incorporating two companies in a holding structure in Germany. This article focuses on the creation of an Opening Balance Sheet from the bookkeeping software.

In follow-up post(s) I'll continue with further bookkeeping of the first invoices and further highlights until finally having both companies ready.

Hi 👋

This is Kai Mindermann, the CEO of NuInnovate - with the vision of creating a world where every improvement serves a meaningful purpose. Just wanted to quickly say: Enjoy your day!

Overview

Any corporation is required to do double-entry accounting (Doppelte Buchhaltung), create a balance sheet (Bilanz) and create an annual financial statement (Jahresabschluss).

A balance sheet is always based on a specific date and period. To be able to confirm it, it is usually compared to the previous balance sheet. Yet the first one is special, as there is nothing previous to compare to!

After you have informed the tax office about the founding of your company by sending them the filled out Questionnaire for tax registration (Fragebogen zur steuerlichen Erfassung), they will ask you to provide more information (if you have not already sent it along). Among that is the so-called Opening Balance sheet (Eröffnungsbilanz).

There are many articles which mention how you create one for a GmbH manually as it really does not contain a lot of entries. Yet, there are only few resources which describe how to create it based on the bookkeeping software. Most articles handle only the creation of the opening balance sheet for a new year or the closing balance. Also, many do not describe how to electronically transfer it to your tax office via Elster!

Opening Balance Sheet Basics

How should the opening balance sheets look like? In the following I provide you with two opening balance sheets. One for a common GmbH where all the subscribed capital is fully called in, as in the case of my Holding GmbH. The second case is for a GmbH, where only half of the subscribed capital is called in, as in the case of the Operative GmbH. I also provide the required bookings based on the Standardkontorahmen (SKR) 04.

Opening Balance Sheet for Holding GmbH (25,000€ Fully Called)

| Aktiva (Assets) | Passiva (Liabilities and Equity) | ||

|---|---|---|---|

| B. Current Assets | €25,000.00 | A. Equity | €25,000.00 |

| II. Receivables and Other Assets | €25,000.00 | I. Subscribed Capital / Capital Account / Capital Shares | €25,000.00 |

| Capital Contributions Called and Outstanding | €25,000.00 | Subscribed Capital (Corporations) | €25,000.00 |

| Balance Sheet Total, Total Assets | €25,000.00 | Balance Sheet Total, Total Liabilities and Equity | €25,000.00 |

More about the balance sheet structure can be found in§ 266 HGB.

Assuming your founding date is the 2024-01-14, you need to create the following bookings, based on SKR 04:

- 2024-01-14 Opening Balance (OB) Subscribed Capital 25000 € (Soll)9000:(Haben)2900

- 9000: Balance carried forward, G/L accounts

- 2900: Subscribed Capital

- 2024-01-14 OB Outstanding subscribed capital 25000 € (Soll)1298:(Haben)9000

- 1298: Outstanding contributions to the subscribed capital, called in

- 9000: Balance carried forward, G/L accounts

Notice, that this does not contain the upcoming actual transfer of the share capital. That booking will come later.

Key is that you use the 9000 account, as that will be used by the software for opening balances. If you book on anything else, it will not be visible in the opening balance, but just in a regular balance (e.g. for the closing balance sheet)! It took me a little to figure out this behavior of the software, when I followed other articles which did not use that special account!

Opening Balance Sheet for the Operative GmbH (12,500€ Called, 12,500€ Non-Called)

| Aktiva (Assets) | Passiva (Liabilities and Equity) | ||

|---|---|---|---|

| B. Current Assets | €12,500.00 | A. Equity | €12,500.00 |

| II. Receivables and Other Assets | €12,500.00 | I. Subscribed Capital / Capital Account / Capital Shares | €12,500.00 |

| Capital Contributions Called and Outstanding | €12,500.00 | Subscribed Capital (Corporations) | €25,000.00 |

| Non-Called Outstanding Contributions (deducted as liabilities) | -€12,500.00 | ||

| Balance Sheet Total, Total Assets | €12,500.00 | Balance Sheet Total, Total Liabilities and Equity | €12,500.00 |

More about the balance sheet structure can be found in§ 266 HGB.

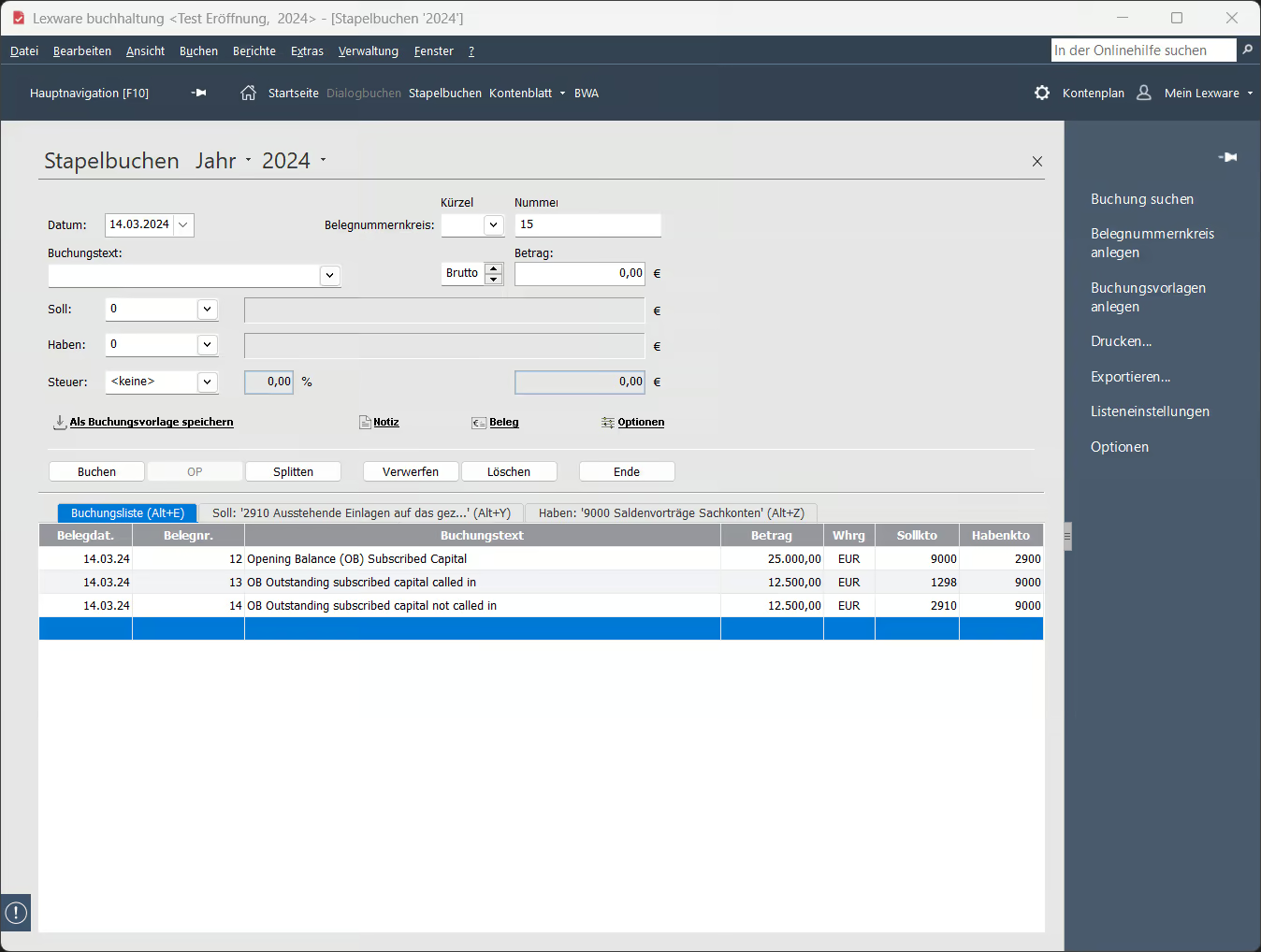

Assuming your founding date is the 2024-03-14, you need to create the following bookings, based on SKR 04:

- 2024-03-14 Opening Balance (OB) Subscribed Capital 25000 € (Soll)9000:(Haben)2900

- 9000: Balance carried forward, G/L accounts

- 2900: Subscribed Capital

- 2024-03-14 OB Outstanding subscribed capital called in: 12500 € (Soll)1298:(Haben)9000

- 1298: Outstanding contributions to the subscribed capital, called in

- 9000: Balance carried forward, G/L accounts

- 2024-03-14 OB Outstanding subscribed capital not called in: 12500 € (Soll)2910:(Haben)9000

- 2910: Outstanding contributions to the subscribed capital, not called in

- 9000: Balance carried forward, G/L accounts

In the following screenshot you see all those three bookings as they are represented in Lexware Buchhaltung 2024:

Notice, that this does not contain the upcoming actual transfer of the share capital. That booking will come later.

Key is that you use the 9000 account, as that will be used by the software for opening balances. If you book on anything else, it will not be visible in the opening balance, but just in a regular balance (e.g. for the closing balance sheet)! It took me a little to figure out this behavior of the software, when I followed other articles which did not use that special account!

Submit the electronic balance sheet (E-Bilanz) via Elster

Depending on which software or tool you are using for your bookkeeping, it might have a module allowing it to directly communicate with Elster.

As I started with a desktop software, Lexware Buchhaltung, I'll provide you with some screenshots for the creation of the opening Balance and the settings I made:

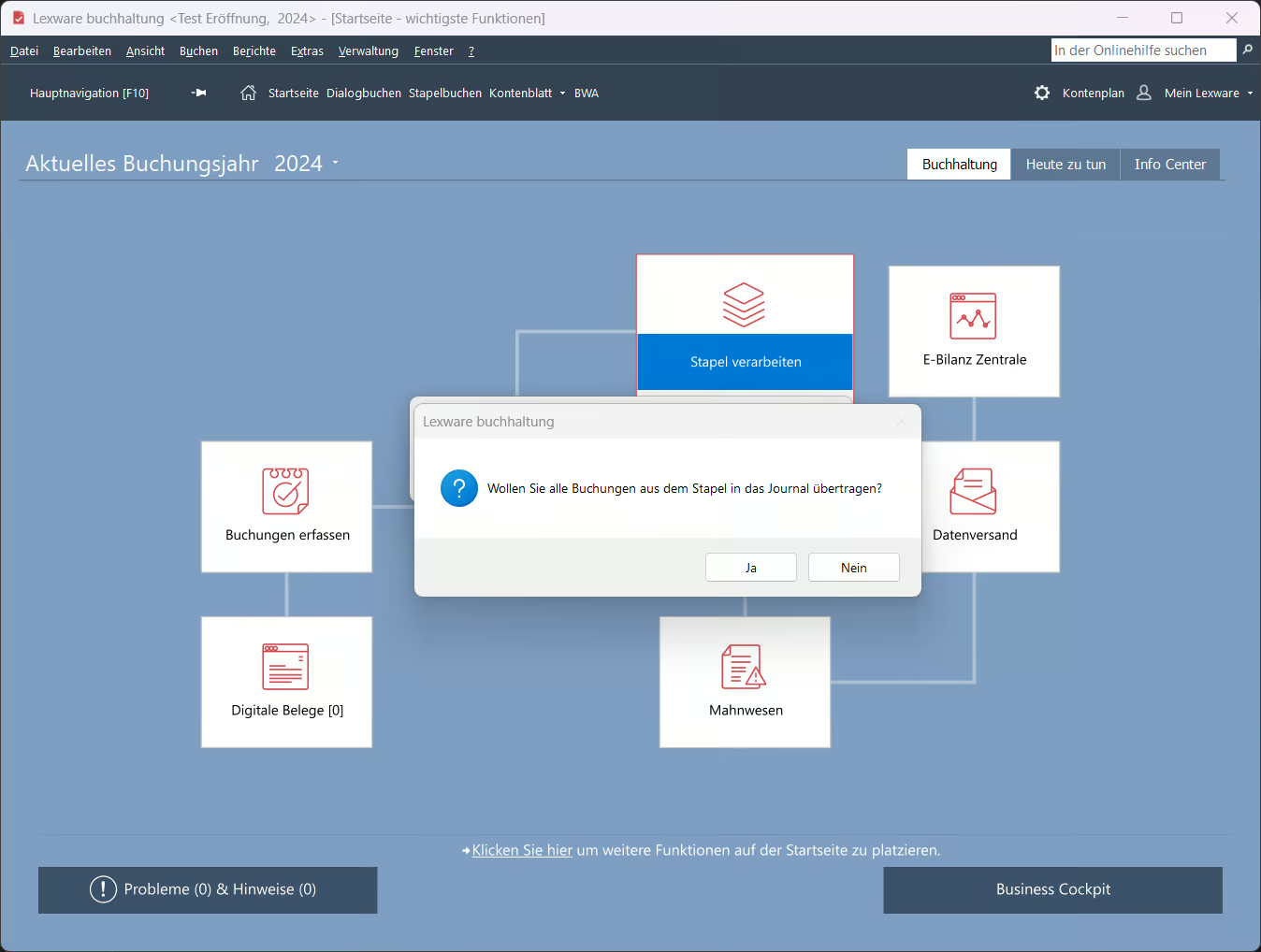

Make sure that all required bookings are carried over from the batch:

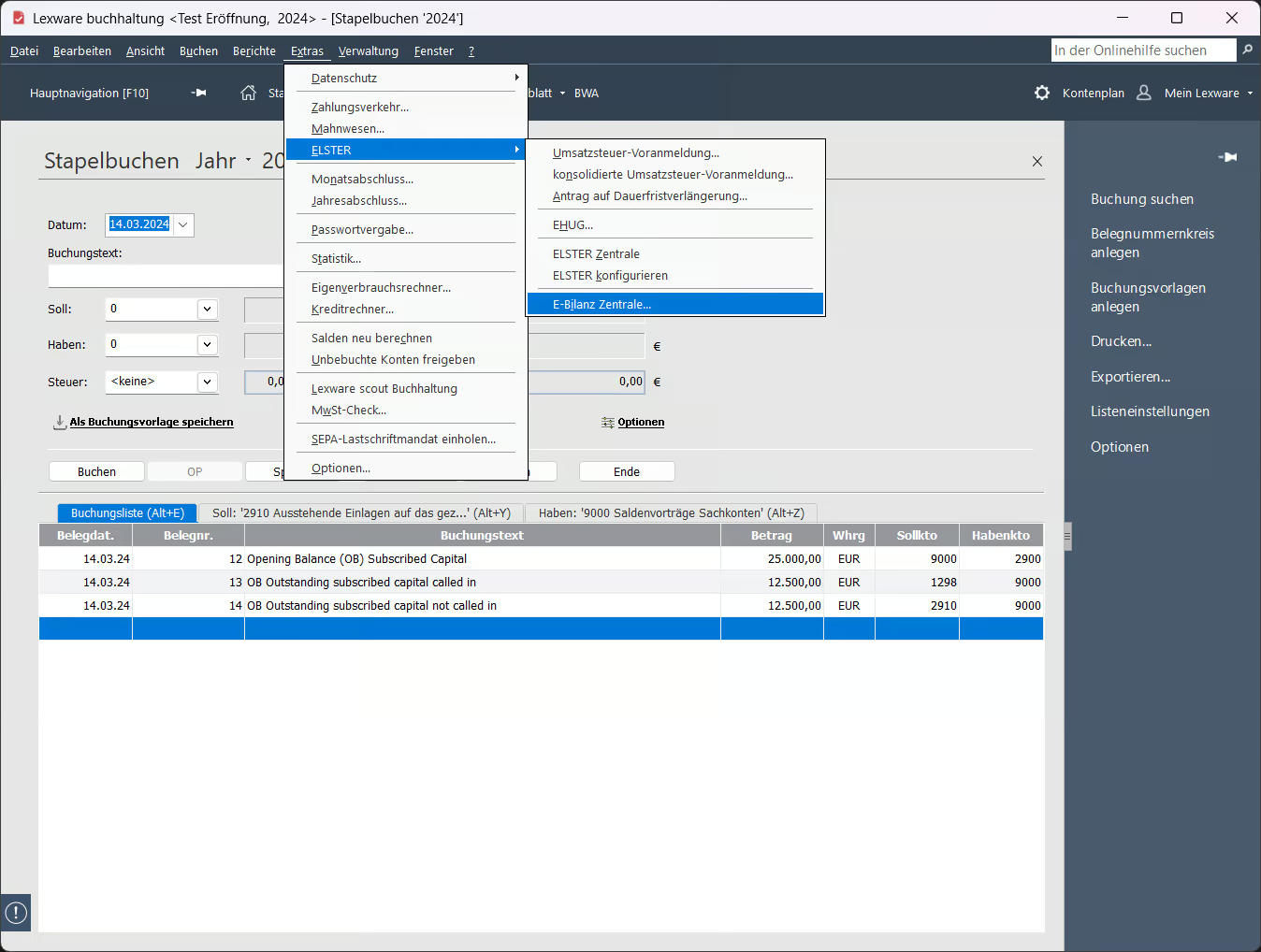

Navigate in the menu to E-Bilanz Zentrale:

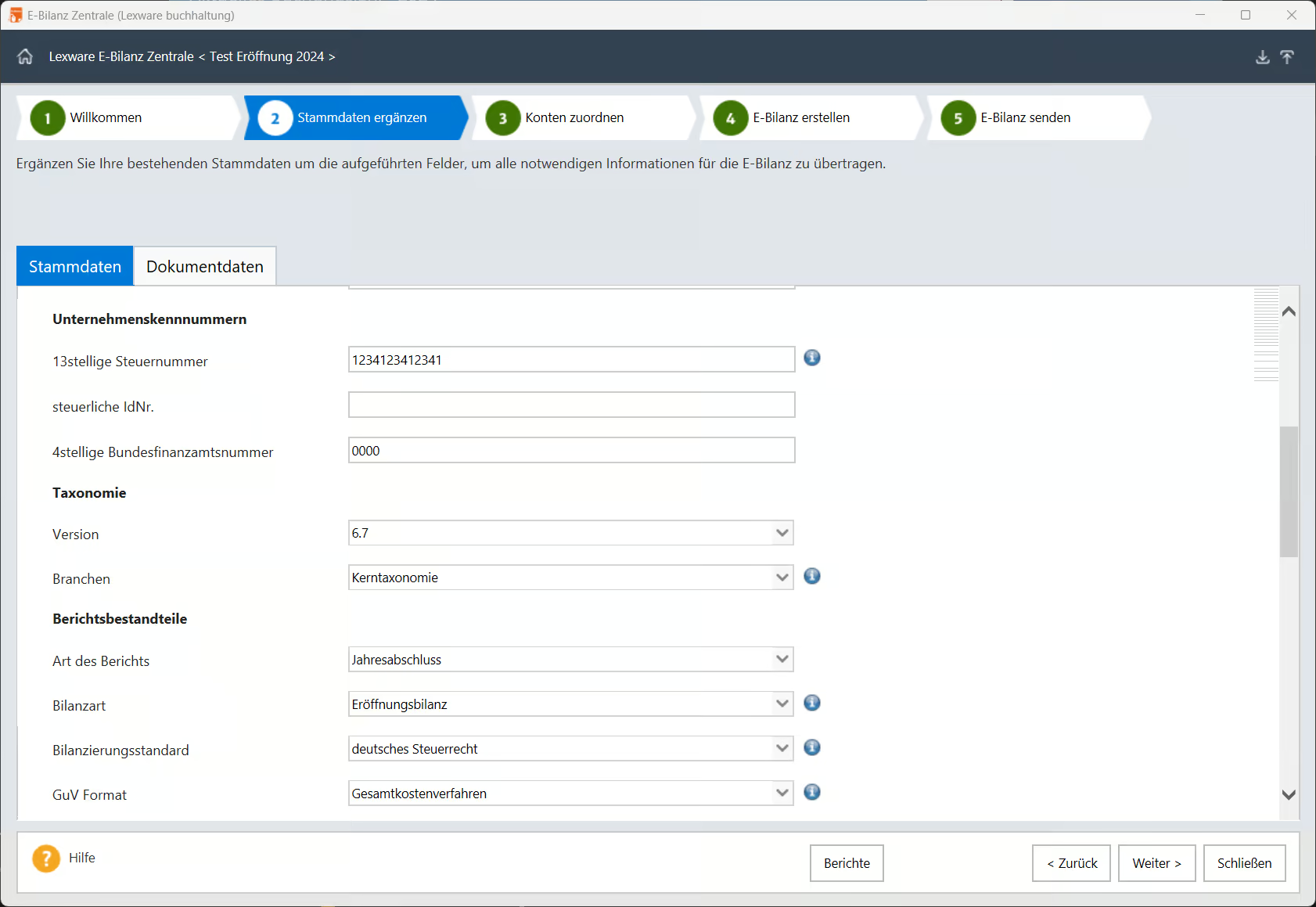

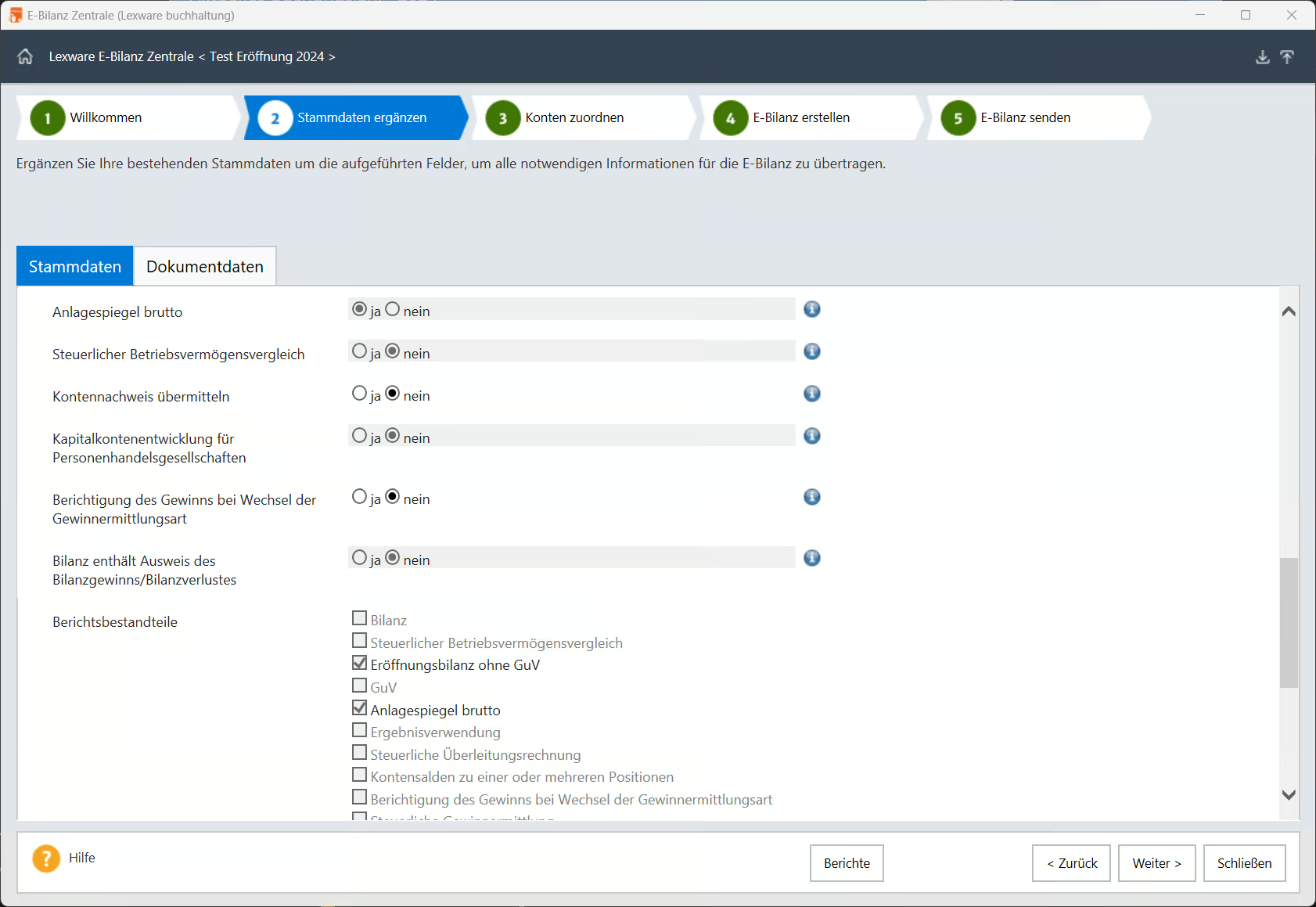

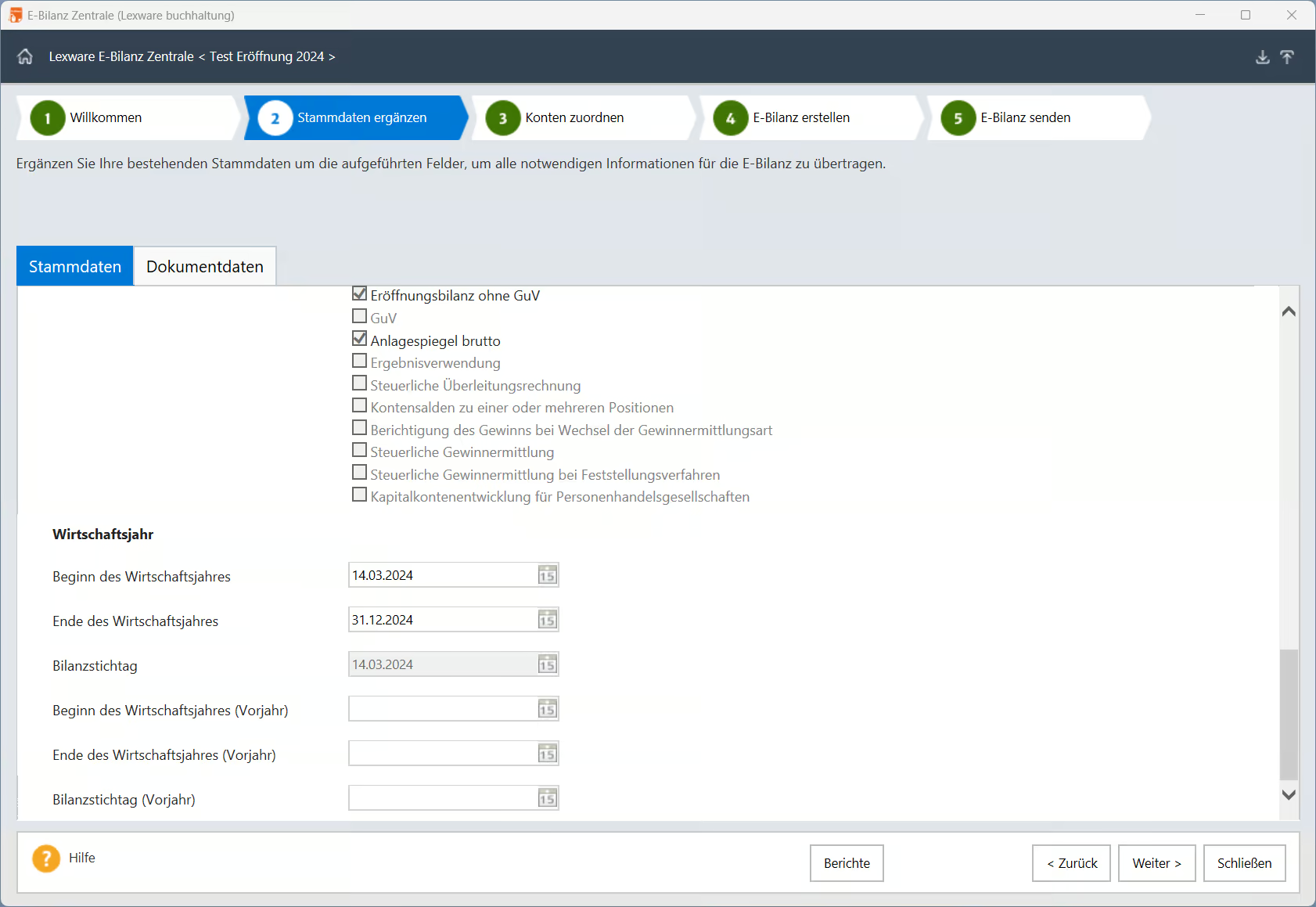

Adapt the company master data as required:

Of course, you need to set the kind of balance sheet (Bilanzart) to Opening Balance Sheet ("Eröffnungsbilanz"). Take special care of the field Beginn des Wirtschaftsjahres, you can use this to change the Bilanzstichtag to the corresponding date, in our example case the 2024-03-14.

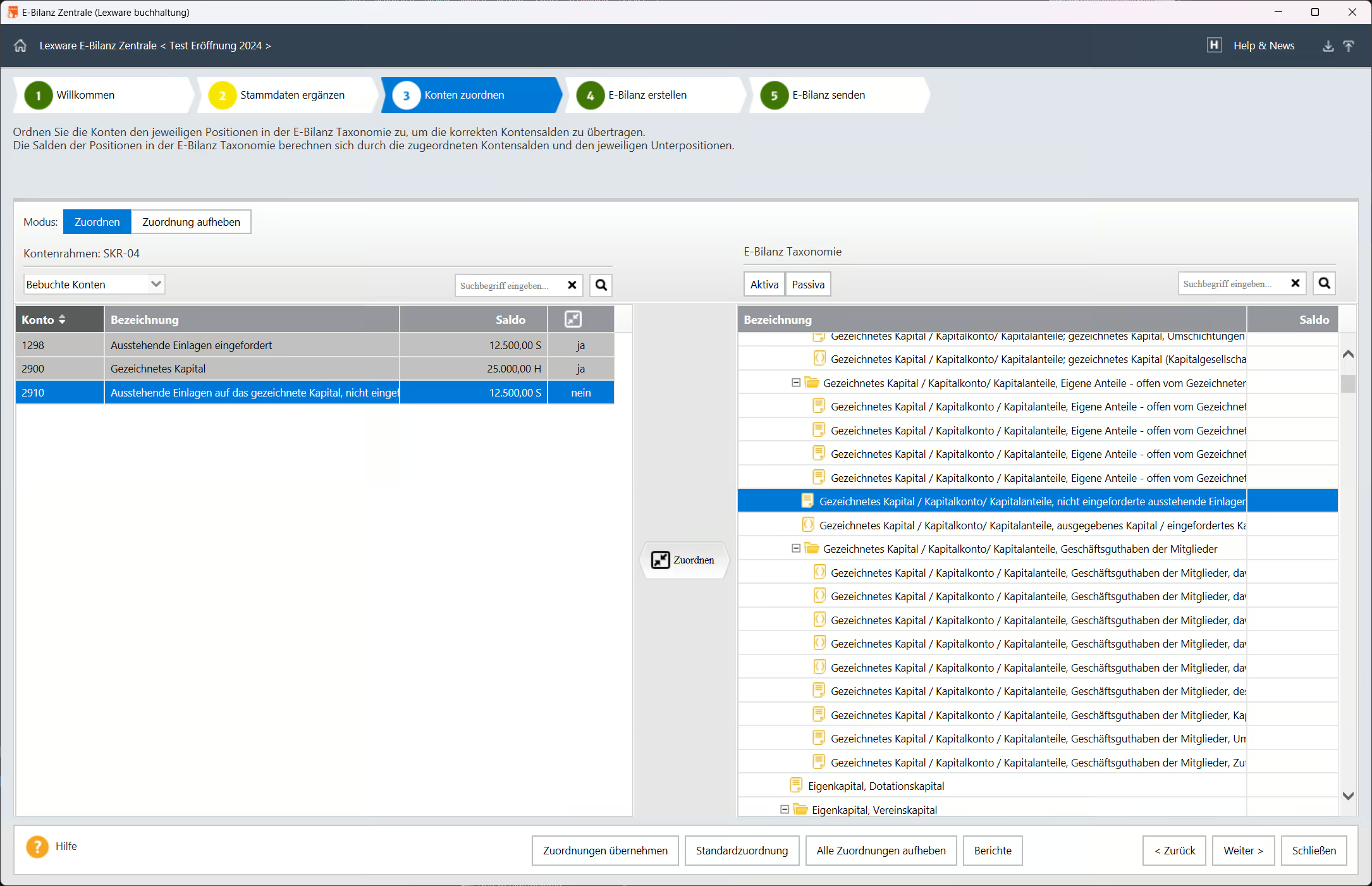

Make sure all accounts you booked on have a mapping to the taxonomy:

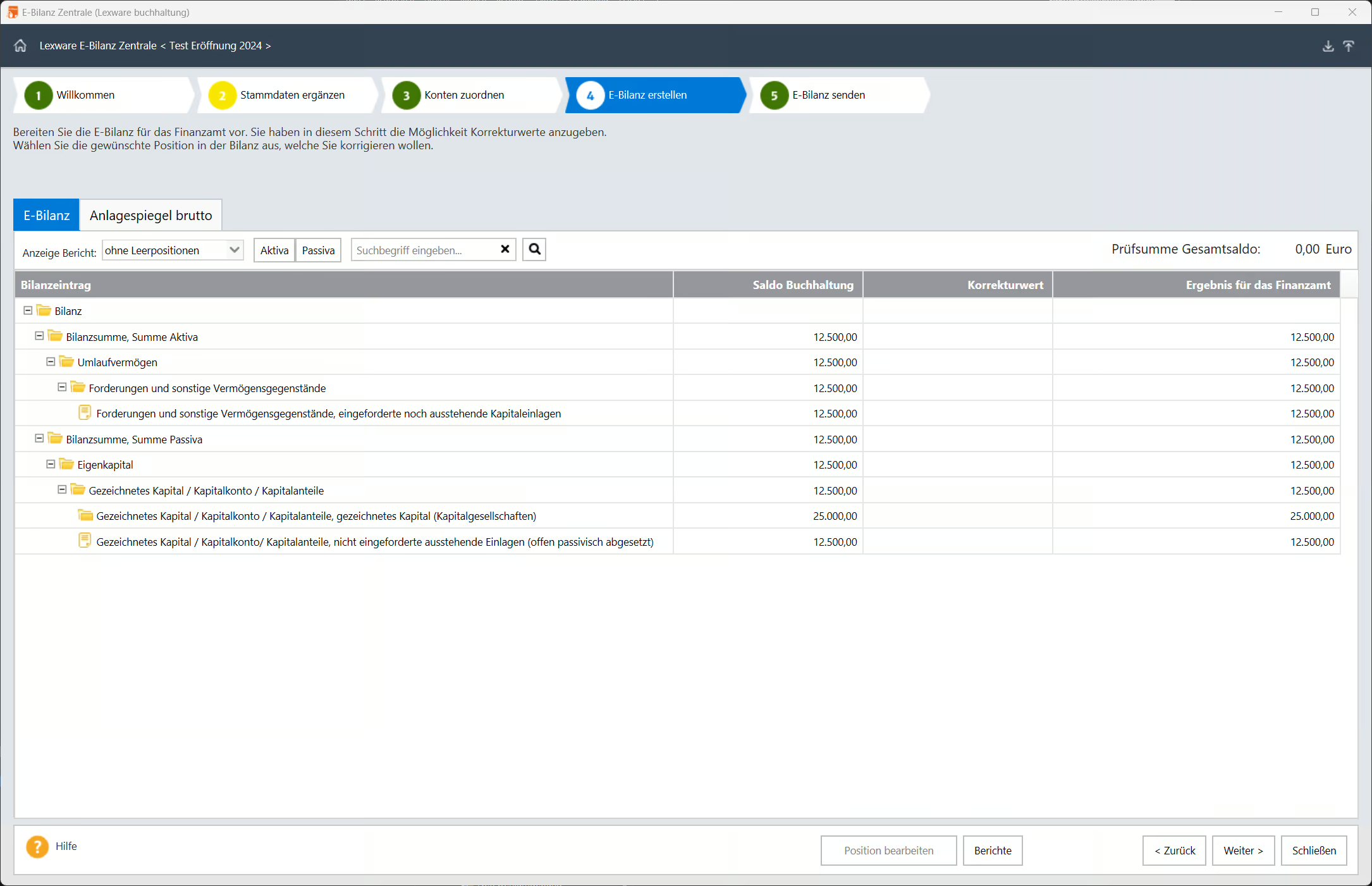

Check the opening balance sheet as previewed by Lexware Buchhaltung E-Bilanz Zentrale:

After you have reviewed everything in the 5th step of the dialog (e.g. that the checksum Prüfsumme Gesamtsaldo is zero), you can go ahead and use your personal Elster Certificate to send the company's opening balance sheet. It's irrelevant who sends it, just that it is sent.

If you did not already receive a tax identification number, as the tax office might be waiting for you to submit the opening balance sheet, you can leave it blank. Just make sure to include the correct number for the responsible tax office.

Other insights about the first bookkeepings

There is a difference between batch bookkeeping (Stapelbuchhaltung) and dialog bookkeeping (Dialogbuchhaltung). Batch bookkeeping does not book it directly on to the accounts or does not write it directly to the main "book" or the journal. If your software allows you to differentiate between these two, keep this in mind when you are looking at reports, they might not show everything that you expect in them. Even nothing could be displayed at all... I'm not saying this confused me for long but definitely had to make sure what is currently selected to have the bookings show up!

How to book the not yet occurred but agreed upon maximum founding costs (see Model Protocol/Model Protocol using video communication which automatically agrees to take over a maximum of 300 € / 600 € of the founding costs)? They are an uncertain liability and can be booked on Other provisions (3070, SKR 04). On the active side it could be booked on Prepaid expenses and deferred charges (1900, SKR 04). Yet, I haven't done this.

I recommend you take a look at DATEV's Standardkontorahmen SKR 04 in preparation for the further bookkeeping, it's freely available for download.

The tax office might ask you again for the opening balance sheet, despite that you have sent it via Elster. It was fine, when I told them that I submitted it already via Elster.

Next steps

So far I already covered a few aspects which I discovered, learned and experienced:

- Introduction, watching videos and researching the holding structure

- Making the actual step of going to the public notary and signing the certificate of incorporation

- Virtual Office/Address and Terminology for the different kinds of addresses and locations for the various forms and documents

- Do I need to be present, physically, at the local trade licensing office to perform the trade registration, despite the form being available online?

- (This article) Creating an Opening Balance Sheet, Eröffnungsbilanz, from the bookkeeping software, correctly.

In the next post(s) I'll highlight the next steps, some of which I did not comprehend quickly in the - for me - necessary detail:

- Does the Holding Company really need to calculate and submit (pay) the sales tax pre-registration, Umsatzsteuer-Voranmeldung (USt-VA) after every quarter, despite not doing a lot other than waiting (for years) for the returns of the operative company?

- Why won't the bank open a bank account for the Operative GmbH after opening one without problems for the Holding Company? (Part 7 of Founding a Company)

- Delayed assignment of VAT ID / USt-IdNr because of possible consolidated VAT group / umsatzsteuerliche Organschaft?

Disclaimer

The content provided in our articles is for informational purposes only and should not be construed as legal or tax advice. Readers are encouraged to seek professional advice from qualified professionals regarding their specific legal or tax situations.